|

At the start of the last economic downturn, the Fed reduced the discount rate to help stressed financial organizations cover expenses. In those circumstances, short-term loans tend to get a bit longer. At the height of the monetary crisis in 2008, loans with the discount rate were as long as 90 days. The reduced rate of return likewise called the discount rate and unrelated to the above meaning is the anticipated rate of return for an investment. Also called the expense of capital or needed rate of return, it approximates present value of a financial investment or business based on its predicted future cash circulation. For instance, an investor anticipates a $1,000 financial investment to produce a 10% return in a year. Because case, the discount rate for valuing this investment or comparing it to others is 10%. The discount rate permits financiers and other to think about threat in a financial investment and set a benchmark for future financial investments. The discount rate is what business executives call a "obstacle rate," which can assist determine if a company financial investment will yield revenues. Organizations thinking about financial investments will use the expense of borrowing today to find out the discount rate, For example, $200 invested against a 15% interest rate will grow to $230. This is valuable if you wish to invest today, but need a specific amount later on. The discount rate is often a precise figure, but it is still a quote. It often includes making assumptions about future advancements without considering all of the variables. For lots of investments, the discount rate is just an educated guess. While, some financial investments have predictable returns, future capital costs and returns from other investments differ. That makes comparing those financial investments to a discount rate even harder. How to finance a second home. Often, the finest the affordable rate of return can do is tilt the odds somewhat in favor of investors and companies. It's the rate the Fed charges banks for over night loans and does not straight impact people. The company sense of the term, however, relates to financiers. It's one method of assessing a financial investment's value. Research reveals that passive investing, where you seek to track the marketplace, carries out much better over time than active or tactical investing, where you are attempting to beat the market. Yet passive investing still takes knowledge. To find a monetary consultant who can help you handle your investments, utilize Smart, Asset's totally free tool. It's free and takes five minutes, tops. Still want to attempt your hand at stock selecting? You can reduce expenses by making your trades through an online brokerage account.

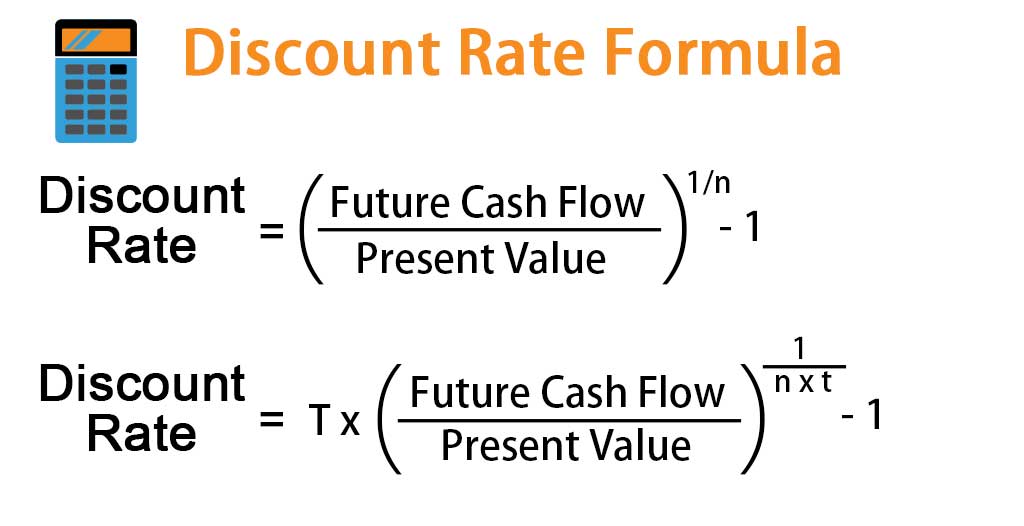

Let's state you're the CEO of Well, Earnings, a growing, Boise-based Saa, https://www.casemine.com/search/us S company that's bound for the stars and thinking of getting investors. One of the very first things you require to do to make your company attractive to financiers is discover your discount rate. Determining your discount rate as a service, however, can be a complex proposition. For both business and investors, discount rate is an essential metric when positioning for the future. An accurate discount rate is important to investing and reporting, in addition to evaluating the monetary viability of brand-new tasks within your business - What is a future in finance. Setting a discount rate is not always easy, and to do it exactly, you need to have a grasp of the discount rate formula. What Happened To Household Finance Corporation for Dummies

Doing it right, however, is essential to understanding the future worth of your business compared to its value now and, eventually, bridging that space. The definition of a discount rate depends the context, it's either defined as the interest rate utilized to calculate net present value or the rate of interest charged by the Federal Reserve Bank. There are 2 discount rate solutions you can use to calculate discount rate, WACC (weighted average expense of capital) and APV (adjusted present worth). The discount rate we are mostly interested in concerns the calculation of your organization' future money flows based upon your business's net present value, or NPV. How to become a finance manager at a car dealership. You need to know your NPV when performing reduced capital (DCF) analysis, among the most typical evaluation techniques utilized by investors to assess the value of purchasing your organization. If your business's future cash flow is likely to be much greater than your present worth, and your discount rate can assist reveal this, it can be the difference in between being appealing to investors and not. The 2nd energy of the term discount rate in company concerns the rate charged by banks and other financial institutions for short-term loans. It's a really different matter and is not decided by the discount rate solutions we'll be taking a look at today.

NPV is the distinction between today worth of a company's money inflows and the present worth of money outflows over a given period. Your discount rate and the time period worried will affect estimations of your business's NPV. NPV is used to measure http://www.timesharetales.com/faqs/ the expenses and advantages, and ultimately the success, of a prospective financial investment in time. http://www.reviewstar.com/tennessee/nashville/legal-financial/wesley-financial-group It takes inflation and returns into account and functions particularly in capital budgeting and investment preparation - there's even a specific Excel function for it. Otherwise, you can calculate it thus: The discount rate aspect of the NPV formula is utilized to account for the distinction in between the value-return on a financial investment in the future and the cash to be purchased today. Some investors may want to utilize a particular figure as a discount rate, depending on their forecasted return - for example, if mutual fund are to be utilized to target a particular rate of return, then this rate of return may be used as the discount rate when computing NPV. You, as the hypothetical CEO of Well, Earnings, might find yourself asked to present the net present value of a solution-building task that requires a preliminary financial investment of $250,000. It is anticipated to generate $40,000 each month of net money flow over a 12-month period with a target rate of return of 10%, which will serve as our discount rate. You can determine it like so: As the hypothetical CEO of Well, Revenue, you 'd first compute your discount rate and your NPV (which, keep in mind, is the distinction between today worth of money inflows and the present worth of money outflows over an amount of time and is represented above by "CF"). Then you can perform a DCF analysis that approximates and discounts the worth of all future capital by cost of capital to get an image of their present values. If this value proves to be greater than the expense of investing, then the investment possibility is feasible.

0 Comments

Currency data are from The Monetary History of the United States, 1867-1960, Friedman and Schwartz, 1963. Bank suspension data are from Federal Reserve Publication, Board of Governors, September 1937. Bagehot, Walter. Lombard Street: A Description of the Cash Market. New York: Scribner, Armstrong & Co., 1873. Board of Governors of the Federal Reserve System. Banking and Monetary Data, 1914-1941. Washington, DC, 1943. Board of Governors of the Federal Reserve System. Federal Reserve Publication. September 1937. Bremer, Cornelius D. American Bank Failures. New York: AMS Press, 1968. Butkiewicz, James L. "The Impact of a Lender of Last Resort during the Great Depression: The Case of the Restoration Finance Corporation." Explorations in Economic History 32, no. Ethical and material accomplishments aside, speed was a vital component of the initial New Deal, just as it will be in a Green New Offer. The initial Reconstruction Financing Corporation was not started by FDR or a New Dealer at all, but by President Herbert Hooverand timeshare selling scams only at the insistence of the country's leading lenders. Two years into the Great Anxiety, the financial slide was becoming an avalanche. Consumer costs had actually fallen by more than 22 percent, and business financial investment was bit more than a third of what it had actually been. The country's jury-rigged banking system was coming apart. In 1930 alone, 1,350 banks were forced to close their doors, and the rate of failures continued to accelerate the next year. Give what you can ... In a meeting with Hoover, the country's monetary magnates pleaded with him to restore the War Finance Corporation (WFC), which had actually been developed to support the economy during and after World War I. The WFC had been an extraordinary federal government intrusion into the economic sector, purchasing war bonds but also lending money "to a variety of business, consisting of utilities, electrical power plants, mining and chemical issues, railways, and banks." Now, the titans of American finance wanted it back. In December 1931, Hoover hesitantly succumbed to the lenders' demand and asked Congress to develop the Restoration Finance Corporationa new War Financing Corporation, by another name. How to find the finance charge. And yet, he could not shoot. The RFC moved warily and secretively under his administrationthe exact opposite of what was needed. The new agency made simply $126 million in loans to 45 banks in the first two months of its existenceand over half of that amount went to just 3 large banks. At the exact same time, the RFC refused to offer cash to the Chicago local workersincluding 16,000 schoolteacherswho had actually not had an income in months and who were clubbed by the city's polices when they westlake financial utah attempted to protest. Hoover insisted on a primitive type of "trickle-down" relief. He did not discover that the approach was flawed. Monetary organizations tended to hang on to their government money, rather than flow it through the economy. Already drowning in debt, taking on loans from the government just made them shakier still. "For a deadly year and a half," Morgan lender Russell Leffingwell later on claimed, "the Reconstruction Financing Corporation continued to lend money to the rely on adequate collateral security and gradually bankrupted them in the effort to conserve them." By the end of the Hoover administration, in March of 1933, simply $197 million in public works had wfg logo png actually been okayed by the RFC and just $20 countless that cash had actually been spent. The American economy had actually collapsed. "The conception of the RFC, for which credit should be accorded to President Hoover, had been good, but it was a year too late. Even when it started, its board, for a time, was completely too shy and sluggish to save the country from the disasters of 1932 and 1933." This assertion, talked to particular certainty, came from Jesse H. Jones, a disgruntled Democratic member of the RFC's bipartisan board. "A couple of billion dollars boldly but carefully lent and expended by such a government firm as the RFC in 1931 and 1932 would have avoided the failure of thousands of banks and averted the total breakdown in organization, farming, and market," Jones concluded. Give what you can ... It was a lesson he would heed, when the brand-new president made him director of the Reconstruction Finance Corporation. archetype of the epic Texan legend, not least because he came from someplace else. Flourishing farmers in Tennessee, Jones's extended family had moved to Dallas when he was a young boy. In his early teenagers, he went to work for a peevish uncle who had constructed an empire in lumber. Jesse inherited business, moved to Houston, and parlayed it into a fortune of his own in property, building and construction, financing, and banking. He would extend his building organization to Dallas, Fort Worth, and even New york city throughout the structure boom of the 1920s, putting up office towers and apartment in Manhattan.

It was Jones who led the drive to dredge the Houston Ship Channel, and transformed the inland city into a major port - What is a consumer finance account. He enticed Texaco, Houston's very first major oil company, to townand to another workplace structure he had actually constructed. He developed the city's leading department shop, its grandest film palace, its finest hotels. He purchased and housed its leading newspaperand utilized it to battle the Ku Klux Klan. Thus numerous future New Dealerships, Jones got in nationwide politics throughout the Wilson administration, when he became a director of the American Red Cross, in charge of offering medical aid and basic relief and comfort to American and Allied soldiers. The Ultimate Guide To Which Person Is Responsible For Raising Money To Finance A Production?

Fifteen years later on, with his almost unerring eye for skill, FDR lit upon Jones as his new RFC chairman even prior to his administration got under method - How many years can you finance a boat. Roosevelt had intended to liquify the RFC, then seen as hopelessly corrupt and useless. Jones convinced him not to, persuading him that it might be an essential tool in the New Deal. In turn, FDR's rely on Jones grew stronger. The Texan was among the three key consultants Roosevelt dealt with practically around the clock, to prepare the opening salvo of the Hundred Days and the New Deal: conserving the banks. Here was absolutely nothing of the "timid and sluggish" that Jones had deplored. I think it's valuable for people to know the difference between "conforming" and "non-conforming" loans. An adhering loan is a mortgage for less than $417,000, while a loan larger than that is a non-conforming (sometimes called "jumbo") loan. There are differences in the qualification standards on these loans. There are a bazillion home loan companies that can approve you for a conforming loan: finding a loan provider for a jumbo loan can sometimes be more tough since the rules are more stringent. There are two various methods to get financed for building a home: A) one-step loans (sometimes called "simple close" loans) and B) two-step loans. Here are the differences: with a one-step building and construction loan, you are selecting the same lender for both the construction loan and the home mortgage, and you fill out all the paperwork for both loans at timeshares wiki the very same time and when you close on one a one-step loan, you are in result closing on the building and construction loan and the long-term loan. I utilized to do lots of these loans years back and found that they can be the best loan in the world IF you're absolutely certain on what your home will cost when it's done, and the specific quantity of time it will require to build. Which one of the following occupations best fits into the corporate area of finance?. Nevertheless, when building a custom-made house where you may not be absolutely sure what the specific price will be, or how long the building procedure will take, this option may not be a great fit. If you have a one-step loan and later on decide "Oh wait, I wish to add another bed room to the third flooring," you're going to have to pay money for it right then and there due to the fact that there's no wiggle room to increase the loan. Also, as I discussed, the time line is extremely important on a one-step loan: if you anticipate the house to take only 8 months to construct (for instance), and after that building is delayed for some reason to 9 or 10 months, you've got major concerns. This is a far better suitable for individuals constructing a custom home. You have more flexibility with the final expense of the home and the time line for structure. I tell individuals all the time to expect that modifications are going to happen: you're going to be building your home and you'll realize midway through that you desire another function or wish to alter something. You require the flexibility to be able to make those choices as they take place. With a two-step loan, you can make changes (within reason) to the scope of the home and add change orders and you'll still be able to close on the home mortgage. I always give people plenty of time to get their homes built. Hold-ups happen, whether it is because of bad weather or other unpredicted situations. With a two-step, will have the flexibility of extending the construction loan. We look at the exact same basic requirements when approving people for a building and construction loan, with a few differences. Unlike the VA loans or some FHA loans where you may be able to get 100% funding and even have absolutely nothing down, the optimum LTV (loan-to-value) ratio we typically deal with has to do with 80%. Significance, if your home is going to have a total rate of $650,000, you're going to need to bring $130,000 cash to the table, or a minimum of have that much in equity someplace. What Was The Reconstruction Finance Corporation Fundamentals Explained

One popular concern I get is "Do I require to sell my existing home before I get a loan to construct a new house?" and my response is constantly "it depends." If you're seeking a building and construction loan for, let's say, a $500,000 home and a $250,000 lot, that indicates you're trying to find $750,000 total. So if you currently live in a house that's settled, there are no difficulties there at all. However if you presently reside in a house with a mortgage and owe $250,000 on it, the concern is: can you be approved for a total financial obligation load of $1,000,000? As the home loan guy, I have to ensure that you're not taking on too much with your debt-to-income ratio (How long can you finance a used car). Others will be able to live in their current home while structure, and they'll offer that home after the brand-new one is completed. So the majority of the time, the concern is just whether you sell your current house prior to or after the new home is constructed. From my point of view, all a lending institution truly requires to understand is "Can the client make payments on all the loans they get?". What is a cd in finance. Everybody's financial scenario is various, so simply remember it's all about whether you can handle the overall quantity of debt you get. There are a couple of things that a lot of individuals do not quite comprehend when it comes to construction loans, and a few errors I see regularly.

If you have your land currently, that's excellent, but you definitely don't require to. In some cases individuals will get approved for a construction loan, which they get thrilled about, and in their enjoyment while designing their home, they forget that they have actually been authorized approximately a particular limitation. For instance, I as soon as worked with some customers who we had approved for a construction loan approximately $400k, and after that they went happily about designing their home with a builder. I didn't hear from them for a few months and began questioning what happened, and they eventually returned to me with a completely various set of plans and a various contractor, and the total cost on that house was about $800k. I wasn't able to get them financed for the brand-new home because it had actually doubled in price! This is especially essential if you have a two-step loan: timeshare relief consultants sometimes people believe "I'm received a substantial loan!" and they head out and buy a brand-new vehicle. which can be a huge issue, since it alters the ratio of their earnings and financial obligation, which suggests if their qualifying ratios were close when obtaining their building loan, they may not get approved for the mortgage that is required when the building and construction loan develops. Don't make this mistake! This one might appear very obvious, but things happen often that make a bigger effect than you may anticipate. He remedied it fairly rapidly, however sufficient time had actually passed that his loan provider reported his late payment to the credit bureaus and when the building and construction procedure was finished, he couldn't get financed for a home loan due to the fact that his credit history had dropped so significantly. Despite the fact that he had an extremely large income and had lots of equity in the deal, his credit https://www.openlearning.com/u/stanton-qg5ysl/blog/10EasyFactsAboutWhichPersonIsResponsibleForRaisingMoneyToFinanceAProductionExplained/ ranking dropped too dramatically for us to get him the home mortgage. In his case, I was able to help him by extending his building and construction loan so he could keep the house long enough for his credit rating to recuperate, however it was a significant hassle and I can't constantly depend on the ability to do that. A client checks out the biller's site. After consumer authentication (user name and password), the biller's Web server presents the billing details. The customer evaluates the bill. When the customer schedules a payment, your website collects the payment info, and using Payflow, safely sends it to Pay, Pal for processing on the date defined by the client. Pay, Friend prepares the ACH payment details and provides it for ACH submission to the stemming depository monetary organization (ODFI) by electronic transmission over a safe connection. The ACH payments are sent to the ODFI on the customer-specified payment date. The ODFI processes the ACH payment information and digitally provides the info to the ACH network operator (Federal Reserve). The Federal Reserve credits the ODFI's savings account on settlement day for the worth of all ACH debits transferred, and debits the RDFI's savings account for the worth of ACH items received. Pay, Pal then starts a secondary deal to move the cash into your (biller's) bank account. The customer's regular bank statements show ACH payments (What jobs can i get with a finance degree). Merchants are alerted of ACH payments on their bank statements. Merchants use Pay, Friend Supervisor to see status and reports on previously sent payments. If a consumer debit leads to a return for insufficient funds, closed checking account, or other error condition, then Pay, Buddy debits your savings account for the quantity of the return.

Before submitting an ACH payment, you should initially acquire authorization from the consumer to http://augustkggh356.huicopper.com/how-to-import-stock-prices-into-excel-from-yahoo-finance-can-be-fun-for-anyone debit their checking account for the quantity due. For detailed info, describe Summary of Permission Requirements. Unlike the credit card network, the ACH network is unable to provide actual time permission of funds. The Payflow ACH Payment service therefore responds Have a peek here initially to an ACH payment by examining the format and other specific ACH information and returning an approved result. The status of a payment modifications Check over here during the lifecycle of the payment and occurs when Pay, Friend settles the payment with the ODFI and again if either a Return or an Alert of Modification is received. Payment sent Thursday after 7 PM are not sent out for settlement until Sunday at 7 PM. If Monday is a banking holiday, then payments are sent for settlement on Monday at 7 PM. If a payment is not successful (for reasons such as a bad savings account number, insufficient funds, a disagreement, and so on), Pay, Pal gets a return from the ACH network - usually within 2-4 organization days of payment submission - Which results are more likely for someone without personal finance skills? Check all that apply.. For Business-to-Business deals, a business has 2 days to contest a charge. For Business-to-Consumer, the consumer can dispute a charge up to 60 days after the payment was processed. Electronic payments or ACH are a simple method to transfer and receive funds. You likely use ACH transfers everyday and do not realize it. ACH deals simplified our lives, making moving funds more secure, much faster, and simpler. But what does ACH stand for? In this article, we cover what ACH means, how it's used, and examples of ACH transactions so you can comprehend the process of making money or paying costs digitally. ACH is the electronic processing of monetary deals. You have actually most likely used it lot of times in your life. For example, if you have actually received payment by means of Direct Deposit or you have actually permitted a financial institution to debit your represent your monthly payment automatically, you have actually utilized ACH. Discussions between a group of California bankers and the American Bank Association began at this time when both entities recognized the present system (paper checks) wasn't practical long term. They knew it would overload the system and delay payment processing. By 1972, ACH was formed in California. In simply a few brief years, more regional operations appeared, which prompted the formation of NACHA. This company manages ACH but does not operate it - that depends on the Federal Reserve and The Clearing Home (How to finance an engagement ring). Soon after the formation, Direct Deposit began. The U.S Flying Force and the Social Security Administration were the first two entities to utilize it. Due to the fact that personal money loans don't originate from standard lending institutions, they can be perfect for financiers looking for creative financing. likewise known as an owner carryback - is ideal for home that's owned complimentary and clear. Purchaser and seller can prevent the apparently endless paperwork of applying for a home mortgage and the seller might have the ability to carry out a 1031 exchange to defer paying capital gains tax - how many years can you finance a used car. When utilizing this choice, be sure to watch on your general debt-to-income ratio and the change in money circulation. are an excellent method to raise capital for a greater down payment and increase the capital reserve account. Because there might be multiple borrowers in a JV, lending institutions might be more unwinded in their loan terms and provide better interest rates in exchange for the decreased danger. Some financiers prefer to keep their equity intact, with a low loan balance and solid capital. Other rental residential or commercial property owners turn accrued equity into capital with cash-out refinancing, utilizing those funds to acquire extra rentals and scale up the portfolio. Requirements for investment property cash-out refinancing vary from lending institution to lender. The Best Strategy To Use For Which Person Is Responsible For Raising Money To Finance A Production?

Note that from the loan provider's perspective, that's the exact same thing as getting a 25% deposit on the brand-new mortgage. If you have actually owned existing rental home over the past few years, the chances are you have actually constructed up a significant amount of equity from increasing market values. As an example, let's state you bought a single-family rental home 5 years ago with a $100,000 loan quantity. Your cash-out refinancing would yield: $150,000 existing value x 75% new mortgage = $112,500 - $80,000 existing loan balance reward = $32,500 in available capital for extra genuine estate investments. At very first glance, funding multiple rental homes may appear like a difficult dream. However with a little imagination and advanced preparation, it's simple to make that dream come to life. Objective for a personal credit report of at least 720 to increase your capability to certify for more than one home mortgage and to obtain the most beneficial rate of interest and loan terms possible. Be a credible borrower by having personal details and financial efficiency reports of your present rental property prepared ahead of time. How What Is The Meaning Of Finance can Save You Time, Stress, and Money.

Look around for a lender the same way you would go shopping around for an investment property, and deal to bring your loan provider repeat company and recommendations as you continue to grow your rental home portfolio. For several years, you have actually been diligently paying off your personal debt. You have actually finally got a healthy cost savings account. You're funding your 401(k). Everything is working out, however something is still missing out on: You 'd truly like to offer realty investing a shot. The most significant barrier that's tripping you up is the financing procedure. There are always a couple of wrinkles to be straightened out. But if you're thinking about the purchase of residential or commercial property, sort through your various alternatives and make sure to consist of the following. Lots of investors continue to utilize regional banks and credit unions to finance property financial investments, however those are no longer the only alternatives. Not known Facts About How To Finance A Manufactured Home

Rather, the honor of a lot of convenient loaning service has gone to online loan markets like LendingTree, LoanDepot, Quicken Loans, and Rocket Home mortgage. With an online loan market, you don't have to lose time driving from one bank to another and sitting in on great deals of uninteresting conferences, only to hear the same old spiel again. Are you having trouble qualifying for a home loan? Or perhaps the rate of interest you're provided just isn't practical offered your numbers? One option is to hold off for a few more months and stash away more money. If you can put 25 percent down or more, you can save significantly on the interest. Seller funding is a smart alternative that frequently works when a financier can't get a loan from a bank or other standard financing source. In this case, the seller of the propertywhich is often owned free and clearessentially becomes the bank. You take ownership of the property, however then cut month-to-month "mortgage" payments to the previous owner. More About Accounting Vs Finance Which Is Harder

If you attempt to pursue seller funding, you have to get together a wise strategy. Approaching a seller with no details isn't going to inspire his or her confidence. You require to have specific terms composed out and ready to be executed. There's something to be stated for owning a piece of property totally free and clear. You most likely aren't in a position where you're able to purchase a home with cash by yourself certainly. But the good news is, you do not need to. You have the alternative to collect a group of financiers and go in together. Let's state you're interested in purchasing a $200,000 rental home, for example.

This is a terrific method to get your feet damp while spreading out the threat. You never wish to hurry into buying a home. It doesn't matter whether it's going to be your personal residence or a rental. Absolutely nothing excellent ever occurs in property investing when the trigger is pulled too soon. You can save some money and have a more cost effective payment if you choose to buy an utilized vehicle. There are nevertheless, some trade-offs to buying used, too. There are some 0% and other low-rate financing offers offered for pre-owned cars and trucks at much shorter terms, such as 36 months that might minimize your payment if you qualify. Many people go buying a vehicle and discover one they like prior to they think about financing. That's backward. You're most likely to succumb to dealership sales methods and purchase a more pricey automobile than you can manage when you shop by doing this. Rather, get preapproved for a loan with a bank, credit union or online loan provider. With a preapproval, you'll understand how much you can obtain to spend for the cars and truck and what the monthly payment would be. You'll have a loan amount and interest rate that you can use to compare with the funding alternatives from the dealership and other lending institutions. You'll be prepared to make a notified choice when you discover the automobile you desire. Lenders look for a high credit rating for an 84-month loan term, so inspect to see what your credit might be before applying. That way you'll understand which lending institutions may offer you preapproval. With simply a little preparation, you can get preapproved by a bank, cooperative credit union or online lender. Lenders will utilize your creditworthiness to determine the rate of interest they will provide you. Bear in mind that the credit rating for a car loan is a little bit various from other loans. Get your information together prior to you visit a lender or use online. You'll require documents like: Personal information, including name, address, telephone number and Social Security number. Employment Details, such as your employer's name and address, your job title and income, and length of work. Financial info, including your present financial obligations, your living situation, what type of credit you have readily available and your credit rating. Loan info, consisting of the amount you expect to finance and the length of the loan term you want, in addition to any trade-in or down payment details. Store around for the finest vehicle loan rates. If you're buying a car, numerous credit queries made within 14 to 45 days will not hurt your credit score anymore than a single inquiry would. If you succeed in getting preapproved, you'll receive a loan quote that reveals much you get approved for, the interest rate and the length of the loan. You can use this details when you go patronizing the dealership. You'll know how much you can manage to invest in the car. And you'll be able to compare financing deals. If you have less than good credit, a cosigner could help you get approved for a loan that you may not be able to get on your own.

Remember the cosigner is responsible for paying the loan if you don't pay it. That could negatively affect their credit history as well as yours. If the cosigner is a good friend or family member, ensure they know their commitment to the loan. Understand a few financing traps dealerships might use while you're going shopping for an automobile. If you can acknowledge what the dealership is doing, you can avoid paying more than you planned. Research the producer's suggested retail price (MSRP) of the automobile you're taking a look at, and any rewards that might be readily available. The price tag can vary by trim levels and alternatives, so research study the choices you want. When Looking To Finance Higher Education, What Is The Best Order To Look For Funding Sources? A Things To Know Before You Get This

Be cautious of dealership add-ons that are frequently provided at the last of settlement, such as: Nitrogen in the tires, Upholstery and paint security plans, Vehicle service agreements, Window tinting, Window car recognition number (VIN) engraving bundles, Research study your vehicle's worth on websites like Kelley Blue Book and Edmunds to see the market price for a trade-in in your area. If you still owe cash on the car, and particularly if you owe more than the automobile is worth, you could have less working out power. Do not lose sight of how much the vehicle will cost you through the life of the loan - How to finance a home addition. Look at the total cost of the purchase cost plus the overall quantity of interest prior to you settle on a loan term. This where the loan preapproval will help keep you on track. Have an excellent sense of just how much you can borrow and how much you can afford to pay each month considering your other responsibilities. Leasing can be a good option to a https://www.thepinnaclelist.com/articles/how-save-hours-your-life-real-estate-strategy/ longer loan term. You could drive the very same car for a lower month-to-month payment, although leases are typically 36 to 37 months. Prior to you lease, comprehend the pros and cons compared with buying an automobile. One of the reasons is the typical new lease payment is $466, while the average regular monthly payment for a new loan is $569, Zabritski said. Pros and Cons of Leasing vs. Purchasing a Cars And Truck, Payments on a lease are $100 less typically compared to buying, according to Experian. Payments are more for a loan, however when it's settled, you own the car. Throughout the average lease of 36 months, your car will be under complete warranty coverage. You can purchase prolonged service warranties or lorry service contracts. Otherwise, you are accountable for upkeep expenses. You can move to a brand-new automobile at the end of the 36-month lease rather of being locked into a long-lasting auto loan. Leases normally permit 10,000-15,000 miles per year, and you'll pay more for additional miles, either in advance or at the end of the lease. Unrestricted miles when you own the automobile. You'll pay extra for upholstery discolorations, paint scratches, damages, and use and tear above the normal when you turn the vehicle in. Wear and tear could decrease the resale or trade-in value. The value of the car is set at completion of the lease and disallowing high mileage or excessive wear-and-tear, it should not change - What is a finance charge on a credit card. The car's worth may not be as much as you owe on it and can continue to depreciate as the cars and truck ages. The typical rate for new-car buyers is 5. 61% while used car buyers pay an average 9. 65%, according to Experian - What is internal rate of return in finance. You can generally finance a brand-new cars and truck for 24 months as much as 96 months or eight years. The average loan term is 70. 6 months. Utilized vehicles can normally be financed approximately 72 months, although it can depend on the age and mileage of the automobile. The Definitive Guide to How To Finance An Investment Property

If you're purchasing a vehicle, you may need to fund your purchase with a vehicle loan. Auto loan vary in length depending on the needs of the customer. The average car loan length Visit this link might be the most suitable length for your loaning requires. Some people choose longer loan terms because it enables them to make smaller monthly payments. Although the payments are expanded over a longer amount of time, each payment is more cost effective. Let's say you are financing a $30,000 vehicle over 5 years at 3 percent APR without any down payment and no sales tax. Month-to-month payments would cost $539 per month. A bank does not care if somebody has seller funding, she says. What it appreciates is if a customer's credit report is improving, if they can manage the loan and the loan-to-value of the house, among other things. Given that non-traditional financing such as seller funding isn't usually reported to credit companies, making such payments on time might disappoint up on a credit report, she says. So a borrower will require a bank statement, for instance, as evidence that payments were made frequently for the most recent 12 months and on time. "Lenders will also obtain an official benefit from the lender, in this case the previous seller, which is customary with any loan to be settled through the refinance," Mc, Rae says. The credit bureau can add it to the credit report. A renter may wish to end up being a house owner for various factors, consisting of to get out of future rent increases. Buying a home from a proprietor can be one service, with the owner financing the loan, though usually at a higher rates of interest than a conventional mortgage. "Normally speaking, alternative funding is going to have a greater rate of interest," Mc, Rae says. "Due to the fact that the individual financing knows you're in a bind." Here are some examples of when people may wish to utilize seller funding: A veteran with an insolvency need to wait 2 years to get a VA loan, Mc, Rae says. With balloon payments, the buyer makes fixed monthly payments for a short amount of time, normally a couple of years, prior to making a big, lump-sum payment to settle the remainder of the loan. It depends on the buyers to determine how they wish to finance that lump-sum payment, however it typically happens via pulling from cost savings, refinancing the loan, or offering the property. A down payment is a quantity of cash that the purchasers Check out this site utilize to suggest their interest in buying the residential or commercial property. They give this money to the sellers upfront as a "great faith deposit" toward purchasing the home. Typically, deposits range anywhere in Find more information between 3% -20% of the home's purchase price. However, with owner financing, it is not unusual to see bigger deposits used as a reward for the sellers to accept the alternative financing arrangement. The rates of interest on rates on seller-financed residential or commercial properties are also usually greater than you might see with a bank loan. For the most part, it's since the sellers are taking on some danger in funding the property and the greater rates of interest is implied as payment. With that in mind, it's not unusual to see rates of interest ranging from 4% -10%. However, in addition to the interest rate itself, you also need to decide how the interest will accumulate.

Many buyers and sellers prefer this type of loan because it is simpler to monitor for accounting purposes and it implies that the buyers are able to forecast their month-to-month payments. With this kind of loan a low, introductory interest rate is provided for a few years. Nevertheless, after that introductory-rate duration is up, the interest rate adjusts occasionally. When utilizing an interest-only loan, the buyer just makes payments on the interest that accumulates from the loan for a set amount of time. Then, a balloon payment is made in order to pay off the principal loan amount. Rumored Buzz on How To Finance Building A Home

Did you understand the hottest North Florida land for sale typically sells within days of being noted? Do not lose out! Set up your own custom-made residential or commercial property alert so you can be notified of the latest land as they hit the marketplace! Just click the button listed below and choose the kinds of North Florida land you are searching for and conserve your search to start getting notifies today! As a regional specialist, I likewise have access to North Florida land for sale before it strikes the marketplace and can show you more details that is just available in the MLS. If you would like to establish a time to go over your property needs, please totally free to call me contact me at your convenience.

Standard asset-based loaning, specialized junior and senior protected funding, factoring, and financing for domestic and worldwide trade. Americanlisted has classifieds in website Orange Park, Florida for homes and homes., Residential Mortgage Begetter, NMLS # 341112 is an all-in-one property business that gives you the biggest choice of homes for sale, townhouses, condos, and homes for lease, in addition to available land and business residential or commercial properties for sale in Texas and Georgia. com - Economical Owner Financing Land in Florida Are you looking for owner financed land for sale? We provide low-cost land, budget friendly land, and land with owner funding to assist down the course to land ownership. Ford Credit Customer Care & Support is here for you. Golf course, pool, weight room. Find Florida Owner Financed Properties for sale on Loop, Web. If a roofing is older than 15 years, leaking can start anytime, and that is when a roof will have to be replaced or fixed - How old of a car will a bank finance. Zillow has 1,921 houses for sale in Florida matching Owner Financing. 36 each month for 5 years $199 Document Charge? In one of the more recent, finer parts of North Port, near North Port Estates is this terrific residential or commercial property. Paradise Lakes) in Georgetown, Florida, simply steps from the north end of gorgeous Lake. With this increase in threat, the discount rate can now be risk-adjusted appropriately. This chart highlights the decline of capital gradually as an outcome of various discount rates. The other integral input variable for computing NPV is the discount rate. There are many methods for determining the suitable discount rate. Since many individuals think that it is proper to utilize higher discount rates to change for risk or other elements, they may choose to utilize a variable discount rate. Reinvestment rate can be specified as the rate of return for the company's investments on average, which can likewise be utilized as the discount rate. The rate of interest, in this context, is more frequently called the discount rate. The discount rate represents some cost (or group of costs) to the investor or financial institution. All of these costs combine to identify the interest rate on an account, and that rate of interest in turn is the rate at which the amount is marked down. If FV and n are held as constants, then as the discount rate (i) increases, PV declines. To identify today value, you would need to discount it by some rates of interest (i). The rate that member banks charge each other is the federal funds rate and the rate the Fed charges is described as the discount rate.

The discount rate is the rate that the reserve bank actual controls. That is the rate banks charge each other, and is affected by the discount rate. In this manner, the discount rate in tandem with the fed funds target rate become part of an expansionary policy system. The worth of a bond is gotten by discounting the bond's predicted cash streams to today using a suitable discount rate. Therefore, the value of a bond is gotten by discounting the bond's anticipated money streams to the present using an appropriate discount rate. In practice, this discount rate is frequently figured out by recommendation to similar instruments, supplied that such instruments exist. How How To Finance A Second Home can Save You Time, Stress, and Money.

The present timeshare resale companies under investigation worth of an annuity is the value of a stream of payments, marked down by the rates of interest to represent the payments being made at different moments in the future. The $1,000 difference reflects the rate of interest the Fed charges for the loan, called the discount rate. The Fed might utilize the discount rate for expansionary monetary policy. For example, the Fed raises the discount rate. For example, the Fed raises the discount rate. The Federal Reserve uses the discount rate to reduce cash supply They can get hair shampoos and other hair items at a more affordable rate and offer them to consumers at complete rates. Another obstacle is diverting, which is when companies offer to carry members at a cheaper rate rather than pass on savings to customers. A trade rate discount is offered by a seller to a buyer for functions of trade or reselling, instead of to an end user. They can get shampoos and other hair products at a more affordable rate and sell them to consumers at complete rates. Assume a service offers a 10 year, $100,000 bond with an efficient annual rate of interest of 6% for $90,000. The journal entry for that transaction would be as follows: Cash $90,000 Discount $10,000 Bond Payable $100,000 The interest expense each duration is $6,000, and the amortization rate on the bond payable equates to $1,000 ($ 100,000/ ten years). Usually, the amortization rate is determined by dividing the discount rate by the number of periods the business needs to pay interest. That implies that the amortization rate on the bond payable equal $1,000 ($ 100,000/ ten years). All About What Does Pmt Mean In Finance

This site or its third-party tools use cookies, which are essential to its working and needed to accomplish the functions showed in the cookie policy. By closing this banner, scrolling this page, clicking a link or continuing to browse otherwise, you accept our Privacy Policy. A couple of weeks ago, I was in a meeting with about 15 smart property and financing people, a number of whom have Ivy League MBA's (What credit score is needed to finance a car). We invested about 20 minutes discussing and debating the usage of Discount Rates in analyzing real estate financial investments. Considering that there was some confusion amongst the group about how to choose an appropriate discount rate, I've decided to write a post about it. Here goes. In business realty, the discount rate is used in discounted capital analysis to compute a net present worth. The discount rate is defined listed below: The discount rate is used in reduced capital analysis to compute the present worth of future capital. There is not a one-size-fits-all method to figuring out the appropriate discount rate. That is why our conference went from a conversation to a vibrant argument. Nevertheless, a general guideline of thumb for selecting a proper discount rate is the following: * WACC is defined as the weighted average of all capital sources utilized to finance an investment (i. e. debt & equity sources). Utilizing this method, financiers have the ability to make sure that their preliminary investment in the possession accomplishes their return goals. Now that we have meanings and basics out of the way, lets dive into how discount rate rates are figured out in practice and in theory. Not known Details About What Was The Reconstruction Finance Corporation

It can be thought of as the opportunity expense of making the financial investment. The chance cost, would be the cost associated to the next best investment. Simply put, the discount rate ought to equal the level of return that comparable stabilized investments are currently yielding. If we understand that the cash-on-cash return for the next best financial investment (chance cost) is 8%, then we should utilize a discount rate of 8%. Trade credit may be used to finance a major part of a firm's working capital when. A discount rate is a representation of your level of confidence that future income streams will equal what you are predicting today. Simply put, it is a procedure of threat. Therefore, we need to discount future cashflows by a greater percentage since they are less likely to be understood. On the other hand, if the investment is less risky, then in theory, the discount rate should be lower on the discount timeshare trade rate spectrum. Therefore, the discount rate used when analyzing a supported class An apartment building will be lower than the discount rate used when analyzing a ground-up shopping center development in a tertiary market. The higher the Discount rate Rate, the greater the perceived threat The lower the Discount rate Rate, the smaller sized the perceived threat Remember that the level of danger is a function of both the asset-level risk as well as business strategy danger. Whether you must finance your next automobile purchase is an individual choice. Many people finance since they do not have an extra $20,000 to $50,000 they desire to part with. But if you have the cash, paying for the vehicle outright is the most affordable method to acquire it. However to comprehend that, you require to think about a few elements. Overall purchase rate is the biggest effect on how much you'll pay for the cars and truck. It consists of the price of the car plus any add-ons that you're financing. Depending on the state and your own choices, that might include additional alternatives on the automobile, taxes and other fees and guarantee coverage. APR sounds complex, however the most essential thing is that the higher it is, the more you pay with time. Think about a $30,000 auto loan for 5 years with an interest rate of 6% you pay a total of $34,799 for the car. That very same loan with a rate of 9% implies you pay $37,365 for the automobile. The longer you extend terms, the less your regular monthly payment is. But the much faster you pay off the loan, the less interest you pay in general. Edmunds notes that the existing average for auto loan is 72 months, or six years, but it suggests no greater than 5 years for those who can make the payments work. who benefited from the reconstruction finance corporation. If you take out a vehicle loan for eight years, is your cars and truck going to still remain in good working order by the time you get to the last couple of years? If you're not careful, you might be making a large regular monthly payment while you're also spending for car repairs on an older automobile - which of the following can be described as involving indirect finance?. If you have no credit or bad credit, your alternatives for financing an automobile might be limited. However that doesn't imply it's difficult to get an automobile loan without credit. Get everything you require to master your credit today. Numerous banks and lending institutions are prepared to work with individuals with restricted credit rating. And you might be limited on how much you can borrow, so you probably should not begin taking a look at luxury SUVs. One idea for increasing Visit the website your opportunities is to put as much money down as you can when you buy the car. Get everything you require to master your credit today. The Ultimate Guide To What Is A Future In Finance

There are advantages and disadvantages to asking another person to sign on your loan, however it can get you into the credit video game when the door is otherwise barred. Numerous individuals wonder if they should use a personal loan to purchase a vehicle or if there is really any difference in between these types of financing. Individual loans are typically unsecured loans offered over Find more information fairly short-term durations. The funds you obtain from a personal loan can usually be utilized for a variety of functions and, sometimes, that may include purchasing a car. There are some terrific reasons to use an individual loan to purchase a car: If you're purchasing a cars and truck from a personal seller, a personal loan can hasten the procedure. An individual loan and liability insurance might be cheaper. Lenders usually aren't thinking about funding automobiles that aren't in driving shape, so if you're purchasing a project vehicle to work on in your garage during your downtime, an individual loan might be the better option. But personal loans aren't necessarily tied to the vehicle like a vehicle loan is. Because that increases the threat for the lending institution, they might charge a greater interest rate on the loan than you 'd discover with a conventional car loan. Personal loans usually have shorter terms and lower limitations than vehicle loans as well, potentially making it more challenging for you to pay for a cars and truck using an individual loan. to understand whether you are most likely to be approved for a loan. Your credit likewise plays a substantial function in your rates of interest. If your credit is too low and your rates of interest would be excessively high, it may be much better to wait up until you can build or fix your credit prior to you get an auto loan. to discover the ones that are best for you. Avoid using too lots of times, as these difficult inquiries can drag your credit score down with hard questions. The average vehicle loan interest rate is 27% on 60-month loans (since April 13, 2020) - how much to finance a car. The car dealership might provide you money toward your trade-in. A few thousand dollars can imply a more cost effective loan or perhaps the distinction in between being authorized or not. While a https://gumroad.com/aedelyhgho/p/not-known-details-about-how-to-finance-a-tiny-house lot of dealers will assist you request a loan, you're in a better buying position if you walk into the dealer with financing ready to go. Plus, if you're prequalified, you have a good idea what you can get authorized for, so there are fewer surprises. The Of How To Finance A Pool With No Equity

They might charge high interest or sell you an automobile that's unworthy the money you pay. No matter your financial circumstance, always attempt to work with a dealership that you can trust. Different automobiles will bring different cars and truck insurance coverage premiums. Phone to your insurance provider prior to the sale to discuss potential rate changes so you're not shocked by a higher premium after the truth. If you're purchasing a cars and truck, you may require to fund your purchase with a vehicle loan. Car loans vary in length depending upon the needs of the borrower. The average automobile loan length may be the most ideal length for your loaning requires. Some people select longer loan terms since it allows them to make smaller monthly payments.

Let's state you are funding a $30,000 vehicle over 5 years at 3 percent APR without any deposit and no sales tax. Monthly payments would cost $539 each month. If you decide to select a seven year loan, you would now pay of $396 monthly. This $143 distinction can make a significant effect on your regular monthly budget. A seven year loan needs 84 month-to-month payments, while a 5 year term only needs 60 payments. The longer a loan term, the more you'll pay in interest, according to Credit Karma. Long term auto loan are not for everybody. When it comes time for you to select your vehicle loan length, there are some reasons to say no to longer terms, they consist of: Interest expenses Repair costsOwing more than a car is worthNegative equity cycleLet's state you buy a vehicle for $30,000 with either a 60 or 84 month term and a 3 percent APR and no deposit or sales tax.

For 84 months, you would owe $3301 in interest. If a loan term is longer than 60 months, you might end up making cars and truck payments till after your service warranty has actually expired. This means you'll need to pay for repairs in addition to a month-to-month automobile payment. The longer you own an automobile and the more miles you place on it, the less it deserves. He or she will act as the intermediary between you and the loan provider. They will find you loan providers with low deposits, competitive interest rates, and other loan terms which fit your realty investment requirements. When done right, investing in rental homes is a money circulation business. And it's a great investment technique for 2020. The real estate market crash has actually ended up being a distant memory, and home costs are looking healthy again. And a more powerful economy has helped highlight new financiers who are wanting to make genuine estate a part of their investment portfolio. While choosing a fantastic financial investment residential or commercial property is hard enough on its own, once you've found that perfect home or home, how do you set about funding it? A little creativity and preparation can bring funding within reach for numerous genuine estate financiers. Considering that mortgage insurance will not cover investment residential or commercial properties, you'll normally need to put a minimum of 20 percent down to secure conventional financing from a loan provider. If you can put down 25 percent, you might receive an even much better interest rate, according to home mortgage broker Todd Huettner, president of Huettner Capital in Denver. That can be a powerful reward, and a bigger down payment likewise offers the bank greater security versus losing its financial investment. If the investment goes inadequately, you'll lose your whole stake prior to the bank starts to lose any money in the home - what does aum mean in finance. If you don't have the down payment money, you can try to get a 2nd mortgage on the property, however it's likely to be an uphill battle. [READ: Although lots of aspects amongst them the loan-to-value ratio and the policies of the lender you're dealing with can affect the regards to a loan on a financial investment residential or commercial property, you'll want to examine your credit report before trying a deal." Below [a rating of] 740, it can start to cost you additional cash for the same rate of interest," Huettner says. That can range from one-quarter of a point to 2 points to keep the exact same rate." A point is equivalent to one percent of the mortgage. So a point on a $100,000 loan would equate to $1,000. (Here's when it's rewarding to buy points - how long can you finance a used car.) The alternative to paying points if your rating is below 740 is to accept a higher rate of interest. 7 Easy Facts About Which Activities Do Accounting And Finance Components Perform? Explained

" That way, if you have jobs, you're not dead." If your down payment isn't quite as huge as it ought to be or if you have other extenuating scenarios, think about going to a neighborhood bank for funding instead of a big nationwide banks." They're going to have a bit more versatility," Huettner states.

Home loan brokers are another good option since they have access to a broad range of loan products but do some research study prior to choosing one. how much do finance managers make." What is their background?" Huettner asks. "Do they have a college degree? Do they come from any professional companies? You have to do a bit of due diligence." [READ: In the days when nearly anyone might get approved for a bank loan, a request for owner funding used to make sellers suspicious of possible buyers. However, you should have a strategy if you choose to go this path. "You need Website link to say, 'I would like to do owner financing with this quantity of money and these terms,'" Huettner states. "You have to offer the seller on owner financing, and on you." This tactical plan shows the seller that you're severe about the transaction which you're ready to make a genuine offer based upon the useful assumptions that you have actually provided. Financing for the real purchase of the home might be possible through private, individual loans from peer-to-peer financing websites like Prosper and LendingClub, which link investors with individual lending institutions. Simply know that you might be met some apprehension, especially if you don't have a long history of successful realty investments. Realty is a popular method for people to create retirement earnings. In fact, it's now Americans' preferred long-term investment, according to a recent Bankrate research study. Realty's appeal is at its highest level given that Bankrate started carrying out the research study seven years earlier. That popularity partially relies on real estate producing a steady stream of income, as financiers gather a regular monthly rent from their tenants. The What Can You Do With A Finance Major PDFs

And retired people have upside on that income. With time a well-managed home can increase its leas, putting more money into financiers' pockets every month. The residential or commercial property can also increase in worth, so when it comes time to sell and even purchase another home, there's equity that can be tapped. REITs are enormously popular with retired people due to the fact that of their consistent dividends. [READ: Property is generally a long-term video game where the gains tend to come with time. But however you buy realty, you can make money if you follow smart principles of investing. When funding residential or commercial property, make sure you can afford the payments when you get the loan. Last Upgraded on November 6, 2019 by Mark Ferguson Last Upgraded on November 6, 2019 by Mark Ferguson Getting a loan on one or two leasings is not hard if you have excellent credit and a decent task. Nevertheless, numerous banks will inform you it is difficult to get more than four loans. There are ways to get loans on 10, 20 or perhaps 100 homes. There are standard banks that will finance more than 4 properties and portfolio lenders who will provide on several properties if you know where to look. There are even national lending institutions that concentrate on rental home loans who choose to provide on substantial plans of rentals. Don't offer up hope! Regional lending institutions who offer portfolio funding are another choice (my favorite) for financiers. It can take some research study, time and networking https://midplains.newschannelnebraska.com/story/43143561/wesley-financial-group-responds-to-legitimacy-accusations to discover a portfolio loan provider, but they have much looser loaning standards. Portfolio loaning implies the bank is utilizing their own cash to fund offers, and they don't need to utilize Fannie Mae standards. The Best Guide To How Many Years Can You Finance A Car

They permit 20% down on those homes and don't need your life's history to provide you the loan. Loaning Home is the biggest difficult cash loan provider in the United States. They have very competitive rates (below 10%) with The country's leading in rental loans. Rental loans, trip rentals, and business loans. They was among the very first lenders to cater to rental Lending One offers home turning and rental residential or commercial property loans. I have utilized them to finance numerous house flips and they There are some downsides with a portfolio lender. With my local bank, they do not provide a 30 year fixed home loan.

I choose to utilize ARMs with a 30-year mortgage rather of 15-year home mortgages since the payments are much lower, which provides me a lot more capital. I can conserve that cash flow and keep buying increasingly more leasings that make a lot more cash than the 4% or 5% interest rates on the loans. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

April 2022

Categories |

/PNCProspectus2019-5c88003746e0fb00015f901b.jpg)

RSS Feed

RSS Feed